Post

Original Author: Jiawei @IOSG

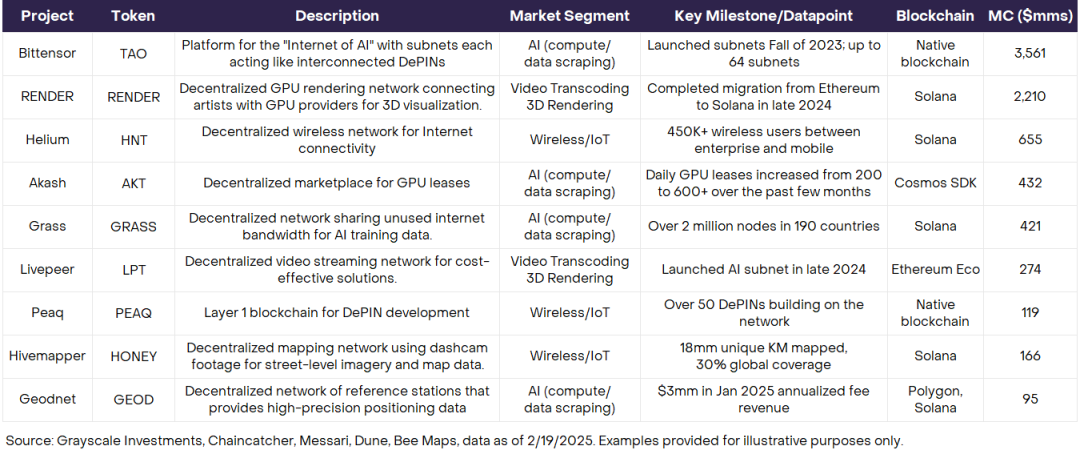

▲ Source: Grayscale

Grayscale wrote a research report on DePIN earlier this year, and the table above shows the top DePIN projects and their market capitalisation. Since the beginning of 2022, DePIN and AI have been being compared as two new directions for crypto investment. However, there doesn't seem to be a single iconic project emerging in the DePIN space. (Helium is a head project, but Helium even predates the concept of DePIN; Bittensor, Render, and Akash in the table are more classified as AI tracks)

In this way, DePIN does not have a strong enough leading project to open the ceiling of this track. There may be some alpha in the DePIN track in the next 1-3 years.

This article attempts to sort out the investment logic of DePIN from scratch, including why DePIN is an investment track worthy of our attention, and proposes a simple analytical framework. Since DePIN is a comprehensive concept that covers a lot of diverse sub-tracks, this article will zoom out a little bit, explaining the concept from an abstract perspective, but still giving some concrete examples.

Why follow

DePIN Investing in DePIN is not a buzz word

First of all, it needs to be clear that decentralising the infrastructure of the physical world is not a fancy idea, let alone a simple "narrative play", but can be implemented. There are indeed scenarios in DePIN where decentralisation can "enable" something or "optimise" something.

Here are two simple examples:

▲ Source: IOSG

In the telecommunications sector, for example, in the U.S. market, traditional telecoms operators (such as AT&T and T-Mobile) often need to invest billions of dollars in spectrum license auctions and base station deployment, and then pay $200,000 to $500,000 for each macro base station covering a radius of 1-3 kilometres. In a 22-year Federal Communications Commission (FCC) auction of 5 G spectrum in the 3.45 GHz band, AT&T invested $9 billion, making it the most expensive operator. This centralised-led infrastructure model has led to high prices for communication services.

Helium Mobile allocates this early cost to each user through community crowdsourcing, and individuals only need to purchase $249 or $499 of hotspot devices to access the network, becoming a "micro-operator", and driving the community to spontaneously network through token incentives, thereby reducing the overall investment. Verizon cost about $200,000 to deploy a macro base station, while Helium was able to achieve approximate coverage by deploying about 100 hotspot devices at a total cost of about $50,000, a cost reduction of about 75%.

In addition, in the field of AI data, traditional AI companies need to pay up to $300 million/year in API fees to platforms such as Reddit and Twitter to obtain training data, and crawl data with the help of Bright Data (residential proxies) and Oxylabs (data centre proxies). Not only that, but it is also increasingly facing more and more copyright and technical restrictions, making it difficult to ensure the compliance and diversity of data sources.

Grass solves this dilemma with distributed web scraping, which allows users to download browser extensions to share idle bandwidth, help scrape public web data, and earn token rewards for it. This model dramatically reduces the cost of data acquisition for AI companies, while enabling data diversity and geographic distribution. According to Grass, there are currently 109, 755, 404 IP addresses from 190 countries participating in the network, contributing an average of 1, 000 terabytes of Internet data per day.

To sum up, one of the starting points of investing in DePIN is that decentralised physical infrastructure has the opportunity to do better than traditional physical infrastructure, or even do things that traditional methods cannot.

As the intersection of Infra and Consumer

, as the two main lines of Crypto investment, Infra and Consumer each face some problems.

Infra projects generally have two characteristics: one is that the technical attributes are very strong, such as ZK, FHE, MPC and other technologies have a high threshold, and there is a certain disconnect in market perception. Second, in addition to the familiar Layer 1/2, cross-chain bridges, staking and other projects that can directly reach end users, most Infra is actually toB. Developer tools, data availability layers, oracles, coprocessors, and so on, are relatively far away from the user.

These two points make it difficult for the Infra project to promote users' mindshare, and the spread is poor. Although premium Infra has a certain amount of PMF and revenue, and is able to self-sustainably go through the cycle, in the market conditions where attention is scarce, the lack of mindshare makes it difficult to do post-listings.

On the other hand, consumers are good at directly facing end users, which has a natural advantage in mindshare's capture. But new concepts can be easily falsified by the market, and may even plummet after a hot switch. Such projects tend to fall into a cycle from narrative-driven to short-term bursts to falsification declines, with short life cycles. Examples include friend.tech and Farcaster to name a few.

Growth, mindshare, and listing are all issues that have been discussed a lot in this cycle. On the whole, DePIN can better solve the dilemma of combining the above two points and find a balance.

-

DePIN is built on the real needs of the physical world, such as energy, wireless networks, etc., and high-quality DePIN projects have a solid PMF and revenue, which is not easily falsified and easily understood by the market. For example, Helium's $30 per month unlimited data plan is obviously cheaper than the plans offered by traditional carriers.

-

DePIN also has the need to use the user side, which can capture mindshare. For example, users can download Grass's browser plug-in to contribute their own idle bandwidth, and Grass has reached 2.5 million users on endpoints, many of whom are non-crypto native users. The same goes for other tracks such as eSIM, WiFi, in-car data, and so on, which are very close to the user.

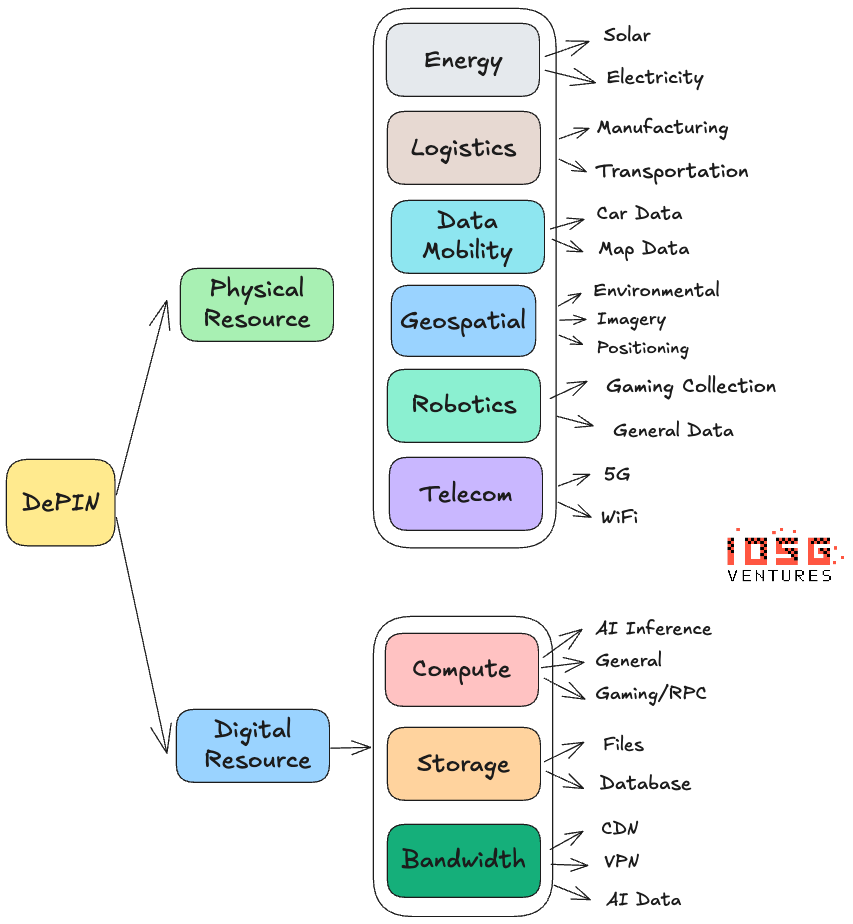

DePIN Investment Framework

▲ Source: Messari, IOSG

direction

Intuitively speaking, 5G and wireless networks are the big markets, and in-vehicle data and weather data are small markets. From the demand side, whether it is a rigid demand (5 G) or a strong demand. And, because 5G has a very large share of the traditional market, even if DePIN can capture a small part of it, the market capacity is quite considerable under the size of Crypto.

According to the greyscale report, the DePIN model is especially suitable for industries with high capital requirements, high barriers to entry, obvious monopoly patterns and underutilisation of resources. Answering the question of PMF essentially depends on two things.

▲ Source: HivemapperOn

the supply side, whether DePIN has done what it couldn't do before, or has outstanding advantages over the original solution (cost, efficiency, etc.). For example, in the map collection track where Hivemapper is located, there are at least three major problems with traditional map collection:

-

Traditional reliance on professional fleets and manual annotation, high cost and poor scalability

-

Google Street View has a long update cycle and low coverage in remote areas

-

Centralized map service providers have a monopoly on data pricing power

Hivemapper, on the other hand, sells dashcams that allow users to collect data, and use crowdsourcing to turn data collection into something that users are doing in their daily driving. Guide users through token incentives and prioritise resources to high-demand areas.

On the demand side, the products provided by DePIN must have real market demand, and it is best to have a strong willingness to pay. In the same example, Hivemapper can sell map data to companies such as autonomous driving, logistics, insurance, and municipalities, and key needs are verified.

When it comes to hardware, Multicoin's 2023 article, Exploring The Design Space Of DePIN Networks, opens with hardware. The author would like to add a few points here.

The timeline for hardware can be summarised as "Manufacture-Sell-Distribution-Maintenance".

#制造

project party designs and manufactures the hardware themselves, or does it use existing hardware? For example, Helium offers both types of self-owned hotspots and can integrate with existing WiFi networks. Or it's a DePIN project for computing and storage, which can directly use existing graphics cards and hard drives, etc.

#销售

clearly marked price of sales means that users will calculate the payback cycle based on the potential revenue. Helium's home mobile hotspot costs $249, and DIMO's in-vehicle data collector costs $1, 331.

How are#分发

distributed? There are many uncertainties involved in distribution: logistics timeliness, transportation costs, and lead times from pre-sales, to name a few. For projects targeting a global scale, inappropriate distribution of designs and tools can significantly slow down the project's schedule.

What

do users need to do to maintain hardware #维护? Some equipment may be depreciated or worn. The simplest example of maintenance is Grass, where users only need to download a browser extension and ask for no additional actions; Or maybe it's a hotspot for Helium, which just needs to be installed and run continuously. It can be more complicated when it comes to solar power and so on.

Combining the above points, the simplest model is Grass's model - directly using the existing network bandwidth, no manufacturing and distribution, no barriers to entry for users, and no sales required, which helps to quickly scale the network early in the project.

Admittedly, projects in each direction have different hardware needs. But hardware is about the friction of initial adoption. In the early stages of the project, the less friction the better, and as the project matures, some friction can lead to retention and a certain degree of binding. For start-up teams, it is necessary to control the path selection and resource investment in hardware, and gradually rather than overnight.

Imagine if it's not easy to go from "manufacturing-selling-distributing-maintaining", then why should users participate unless there is a very strong and deterministic incentive?

Token economy

token mechanism design is the most challenging part of the DePIN project. Unlike projects in other realms, DePIN needs to incentivise various participants in the network at an early stage, so the token needs to be launched at a very early stage of the project. This topic is suitable for a new article to do some case studies, and this article will not be expanded.

In theteam

ratio, the founders need at least one of the following backgrounds: first, they have worked in traditional companies in the field and have rich experience, and are responsible for practical implementation matters such as technology and products, and second, they are crypto-native, understand the token economy and community building, and distinguish the similarities and differences between the preferences and mental models of crypto users and non-crypto users.

Other

regulatory issues, such as the collection of road imagery and data within the country, are obviously very sensitive.

Summary

:Crypto has not really "broken the circle" in this cycle, and it seems that we are still far from the adoption of users outside the circle. The short-term incentives offered by some crypto apps are the reason why users use them, but they can't last. The economic benefits derived from DePIN from the bottom layer have the potential to replace traditional infrastructure on the user side, thereby achieving application sustainability and mass adoption.

▲ Source: Helium

Although the combination of DePIN and reality makes for a long development cycle, we are already seeing some light in the evolution of Helium Mobile: Helium Mobile has partnered with T-Mobile to seamlessly switch user devices to T-Mobile's nationwide 5G network, for example, when the user leaves Helium When the community hotspot ranges, it will automatically connect to the T-Mobile base station to avoid signal interruption. Earlier this year, Helium announced a partnership with global telecommunications giant Telefónica to begin its expansion in South America with the deployment of Helium Mobile 5 G hotspots in Mexico City and Oaxaca. Telefónica's Mexican subsidiary, Movistar, has approximately 2.3 million subscribers, and the partnership connects them directly to Helium's 5G network.

In addition to the above discussion, we also believe that DePIN has two unique advantages:

-

Compared with traditional monopolistic large enterprises, DePIN has a more flexible deployment method and means, and the token model can align incentives within the ecosystem. For example, the traditional telecommunications industry is usually dominated by a few giants and lacks the motivation to innovate. In rural areas, for example, there is no incentive for traditional operators to deploy due to their dispersed populations and low and time-consuming return on investment. And with proper tokenomics design, the network can be encouraged to deploy in places where hotspots are scarce. The same goes for Hivermapper to set higher incentives where map resources are scarce.

-

DePIN has the opportunity to bring positive externalities. From the AI company's purchase of internet data collected by Grass, the self-driving company's purchase of Hivemapper's street-level map data, and Helium Mobile's low-cost data plan, DePIN can actually go beyond the realm of crypto to bring value to real life and other industries, and feed back the entire ecosystem through the token economy. In other words, DePIN tokens are backed by real value, not a Ponzi model.

Of course, DePIN also faces a lot of uncertainties: for example, uncertainty in the time cycle due to operating hardware, regulatory risks, due diligence risks, and so on.

To sum up, DePIN is the track we will focus on in 2025, and we will output more DePIN-related research in the future.

Disclaimer: OKX Orbit content is provided for informational purposes only. Learn more